Fintech and proptech may seem to have equally revolutionized financial and real estate services over the past decade. But this is barely true.

While the former has undergone a significant behavioral shift toward seamless user experience and lean operational structures, the latter is still dominated by slow processes and dated systems. This means, however, that real estate fintech is an untapped area of technological innovation. And those who catch up with it first will take the market lead for years to come.

Proptech & Fintech Defined

Two fancy terms coined no later than a decade ago, both proptech and fintech have their roots in “technology.” The former stands for “property technology” and refers to all disruptive real estate startups and their technological solutions aimed at redefining how the property is sold, managed, and invested in, whereas the latter describes how new technology is used to improve and automate the delivery and use of financial services.

At its most basic, proptech includes three technological movements that are increasingly intertwined:

- Smart real estate, which refers to technology-enabled approaches to building homes and managing them through the smart ecosystem of interconnected sensors and gadgets.

- Construction technology, which encompasses all technological solutions that enhance productivity during the construction phase.

- Shared economy, which entails technology-based platforms facilitating the use of real estate assets, both in the residential (AirBnB) and commercial (WeWork) markets.

Fintech, on the other hand, is often associated with money transfer apps such as Venmo and PayPal, crowdfunding solutions such as GoFundMe, and peer-to-peer lending such as Funding Circle.

Both triggered by acute issues such as the lack of transparency into processes, poor data management, and slow decision-making in finance and real estate, fintech and proptech have naturally entered into a significant crossover referred to as real estate fintech, facilitating the transactions of real estate assets.

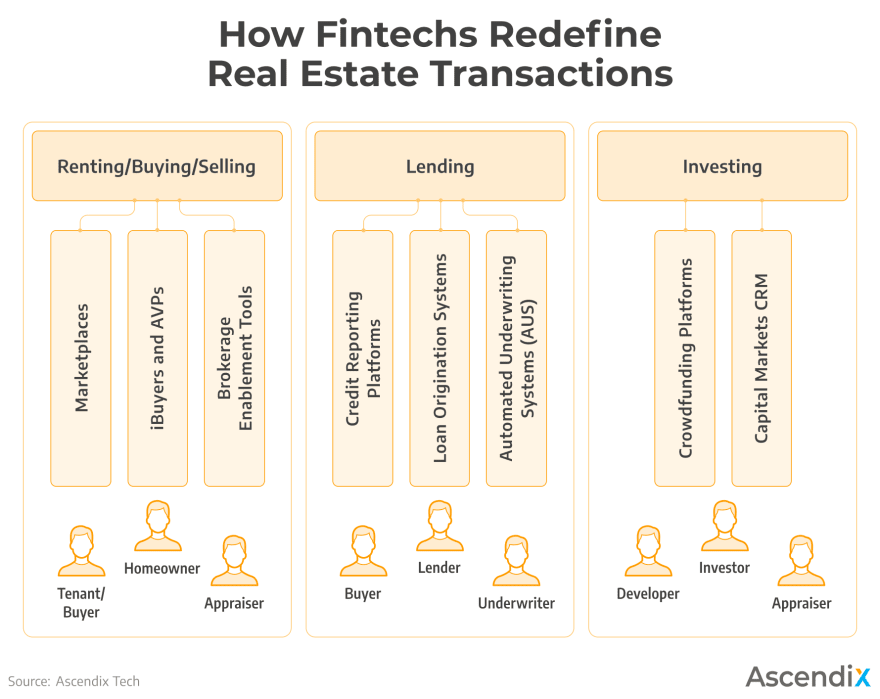

How Real Estate Fintech Companies Reinvent Transactions in Real Estate

Real estate transactions can be divided into three large buckets: 1) renting / buying / selling, 2) lending and 3) investing. Each of these candidly massive chunks of real estate has been suffering from inefficient, opaque systems and processes, making a physical space a frustratingly illiquid asset in terms of speed of sale, probability of sale, and costs associated with that sale.

But not anymore. Or rather not with pioneering real estate fintech companies gradually testing the waters of the change-resilient real estate industry and slowly but surely injecting innovation ideas throughout the whole transaction cycle.

Considering the recent movements in residential and CRE technology, the most probable fintech real estate map looks as follows:

Renting / Selling / Buying

Three major milestones of our life, leasing / selling / buying involves much research and back and forth communication, eventually creating loads of data that one person wouldn’t be able to get a grip of. On the other side of the coin, these opaque processes create a lot of low-hanging opportunities for the below-listed real estate fintech companies and their solutions.

Real Estate Fintech Marketplaces

For a renter, looking for a property can turn into an endless nightmare unless you bring all property information along with photos, price, and neighborhood descriptions in one, preferably, online place.

Partnering with agents and owners, online real estate marketplaces transformed the consumer real estate research experience by creating a standardized place for various firms to display their sale or lease listings and for renters and buyers to search for a desired property. There are two types of such solutions:

- Single family home (SFH) marketplaces like Zillow and Trulia, late so-called PropTech 1.0 firms that came to dominate the US market in the 2000s, offering a simpler and more convenient alternative to a traditional home search experience with greater peace of mind.

- Commercial real estate fintech platforms like LoopNet and Crexi simplifying the search for multifamily and office properties.

At the core of these fintech proptech websites usually lie enhanced data aggregation that captures client’s data provided though chatbots, forms, and face-to-face communication, and Artificial Intelligence that analyses clients’ digital behavior and comes up with smart suggestions that cater to their needs and preferences.

Real Estate Fintech iBuyers and Automated Valuation Platforms

For the prospective homebuyer and seller wanting to upsize or downsize, looking for properties is just as troublesome. The concerns are doubled due to the tremendous uncertainty throughout the valuation process: sellers, when they take an offer, are often hesitant about whether they have asked for the best price, whereas buyers always want to make sure they’re not paying too much.

The fog around the sensitive price question is easily cleared by iBuyers, or “instant buyers” – fintech real estate companies that use algorithms and technology to buy and resell homes quickly.

By leveraging big data and AI to fuel automated valuation models (AVMs) which take hundreds of different factors into account, iBuyers like Opendoor and Offerpad can make a quick and well-informed offer on a house in a matter of seconds.

Incorporating LegalTech such as smart contracts, these outlets eliminate middlemen from the arduous transaction chain, thus dramatically reducing fees for buyers and sellers alike. Considering the tremendous potential of AVM in the home valuation process, the fintech proptech model of iBuyers can be just as helpful for appraisers as they are for home buyers and sellers.

Key features of iBuyers

- Quick, secure way to sell/ buy a home

- Home values are calculated by Automated Valuation Models that instantly process large amounts of data about a home to arrive at an offer price

- No middlemen in transactions thus no extra fees and commissions.

Brokerage Enablement Tools

Brokers are the luckiest stakeholders in the marriage of fintech and proptech, as they can leverage both the above-mentioned solutions (marketspaces for listing marketing and iBuyers for property valuation) and numerous other brokerage enablement tools like CRM systems (AscendixRE, Salesforce, Dynamics 365), marketing collateral generation tools (Composer, Buildout), and secure deal and collaboration rooms (MarketSpace).

However, with the recent real estate shift toward platformization (source), it makes sense to have all these solutions interconnected in one ecosystem rather than leveraging them one by one. This is what Ascendix has done for 26 years and is still doing today.

We have partnered with the big names in the real estate industry like JLL and Colliers and developed custom solutions for their brokerages on top of our core products AscendixRE and Marketspace, as well as Dynamics 365.

If a marketing tool like Marketspace is connected to a Customer Relationship Management system, it can benefit from form fill technology and e-Signature capabilities to prepopulate forms and documents with the data already existing in the form thus dramatically improving broker efficiency.

Lending

In real estate fintech, lending services revolve around mortgages – loans issued by banks or other financial institutions to help a borrower purchase a property. Traditionally, there are at least 3 distinct steps in the mortgage loan process, each taking weeks:

- Application – the first application of the borrower when they are asked to provide, usually as a hard copy, documentation showing their income, savings, debts and any other information that may pertain to your finances – this step takes about a week.

- Underwriting – the most tedious process of assessing the financial risk of lending money to the borrower and evaluating the property – from a week to a few months if additional information is required

- *Closing *– the final step when the borrower receives a Closing Disclosure discussing the final details of the loan, including the loan amount, interest rate, estimated monthly payment, etc. – from 3 days to a week.

Overall, from when the lender receives a mortgage application to the time the loan is disbursed may well pass 52 days, according to Ellie Mae.

However, with the infinite potential of fintech in real estate, a traditional outdated procedure where people still have to fill in hard copy forms and are being asked to provide physical copies of their bank statements can be easily flipped to a completely digital experience where lenders can check your information digitally and approve you for a home loan in less than an hour:

This becomes possible with the following real estate fintech solutions:

Credit Reporting Platforms

Credit risk real estate fintech platforms aim to automate the very first step in the loan origination process – credit reporting. These solutions usually partner with credit reporting bureaus like TransUnion or Equifax to help lenders gain a complete understanding of their client’s credit background before moving forward with negotiations.

To come up with precise analytics, credit risk fintech real estate apps leverage custom credit scoring formulas, risk alert features, and in-depth and predictive analytics programming.

A good illustration of how credit reporting data may be supplied to lenders is Hazu – a quick data provisioning solution that integrates with the lender’s on-site system through a custom-built end interface in order to allow every type of user to easily access, subset, and export the exact data they needed.

It is also imperative that such credit real estate fintech platforms have robust visualization capabilities like those we built in the custom Salesforce CRM for Source Energy Partners.

Key features of Credit Reporting Platforms:

- Integration with reliable credit data providers like TransUnion or Equifax

- Real-time data provisioning through a built-in interface or separate solution

- Enhanced data management and analytics

- Data visualization capabilities

Loan Origination Systems

Developed either for quick loans for retail customers, through mortgage origination processes, or complex business loans for SMEs or corporations, these comprehensive fintech real estate tools will run all stages of the lending process starting from data collection all the way to deal closing – automating all the steps in between.

The main benefit of such proptech fintech platforms is not just collecting applications but automating processes that are normally done by office staff. For example, loan origination tools like a US-based startup Cloudvirga can perform complex calculations at the point of sale to create underwriter-ready loans, while others like Lender Price provide real-time analytics to manage pricing for conforming, non-conforming, qualified and non-qualified mortgages, portfolio, and specialty loans. Thereby these real estate fintech platforms significantly reduce the time to close loans and provide a better customer experience.

Considering the emerging proptech trends around SaaS and data accessibility, it is also vital that the loan origination system is connected to the cloud and integrated with other disparate systems existing within the organization, thus allowing lenders, appraisers, and underwriters to collaboratively work on a loan and access needed data from anywhere anytime.

This is what Ascendix did for a few lending companies on our portfolio who used to struggle with chaotic systems and databases not having a single view of the customer, right until we designed and implemented custom loan origination platforms for them, leveraging cutting-edge cloud and analytics technologies.

Key points of Loan Origination Systems:

- The complete end-to-end loan solution automating all steps in the lending process

- Automated workflows where tasks are routed to responsible parties: lenders, appraisers, and underwriters

- Integration with 3-rd party systems

- Cloud-based solution to allow all parties to operate online

- Digital document processing and e-Signature capabilities like those we custom-built in MarketSpace

- These real estate fintech platforms should also have a mobile solution providing a convenient loan application experience for your customers.

Automated Underwriting Systems (AUS)

Unlike loan generation systems automating all steps in the loan processing cycle, these fintech real estate platforms focus exclusively on underwriting. They utilize machine learning and AI, as well as business rules manually defined by the underwriter, to analyze a client’s financials (such as credit score and income) in addition to the overall value of the property they are looking to purchase (usually determined by an appraiser). From there, the system decides whether to approve a loan application or refer it to a manual underwriter.

Key points of Automated Underwriting Systems:

- Extract data and process documents

- Leverage AI and machine learning to compare borrower information against employment and credit score databases

- Flag any inconsistencies and refer them to a manual underwriter

- Generate property valuations without the need for official appraisals

- Reduce fraud incidents

Investing

The third multi-trillion-dollar bucket of real estate, investing is a complex, multi-step process often obscured by the legacy systems’ inefficiencies. Here are several real estate innovation ideas for those considering addressing these imperfections with the marriage of proptech and fintech.

Online Real Estate Fintech Platforms for Crowdfunding

Real estate fintech crowdfunding is a relatively new way to invest in commercial or residential real estate which gave rise to real estate crowdfunding platforms (aka crowdfunding websites like CrowdStreet and DiversyFund).

The whole beauty about these online real estate fintechs is that they expose everyday investors to assets traditionally reserved for the wealthy by pairing individual investors with developers. This still requires investing capital, although less than what’s required to purchase real estate outright and without the hassles of owning, financing, and managing properties.

Since online fintech real estate crowdfunding platforms are mainly aimed at the individual investor, they should have a user-friendly interface, easy navigation, investment tracking, ID verification, Know-Your-Customer modules, as well as machine-learning-powered chatbots and mobile applications. It is also important to implement document management, reporting, and e-Signature modules, like Composer, one of the main real estate solutions in the Ascendix product family.

Main features of Crowdfunding Platforms:

- Big target audience as crowdfunding offers much more affordable investment opportunities than purchasing a property

- Customer-friendly interface and functionality: investment tracking, ID verification, Know-Your-Customer modules, and machine-learning-powered chatbots

- Document management, reporting, and e-Signature modules.

Real Estate Capital Markets CRM

Another untapped area for the proptech fintech innovation is real estate capital market management. For capital markets firms sourcing investment opportunities and matching those with suitable investors involves multiple chains of communication, both past and present, and loads of data usually unequally spread within the organization’s systems.

To manage such an intricate infrastructure, capital market firms need a core system that would unite all workflows and disparate processes under one hood. And aspiring fintech real estate companies are well positioned to do this by incorporating an all-in-1 Customer Relationship System specifically tailored to the real estate investing transactions.

Here are examples of features we implemented in our AscendixRE CRM for Capital Markets and derivative custom solutions for our clients:

- Detailed profiling of lending preferences: the client’s needs, asset type, occupancy, etc.

- Detailed profiles of Capital Sources and their categorization by Capital type, Property type, Debt/Equity type, equity investment size, geographies, and your custom fields.

- A 360-degree view of the client across multiple asset classes and geographies

- Salesforce-powered data visualization dashboards.

Depending on the capital markets firm nature, additional modules for advanced search (Ascendix Search), document management, or team collaboration may be required.

Why Real Estate Fintech is the Emerging Source of Wealth and Opportunity

Although proptech and fintech have both been the hot topics on the business agenda for the last decade, it would be fair to say that proptech disruption was much inspired by the advancement in the financial services industry, which was once prone to slow, manual workstreams and grounded by physical infrastructure, just as real estate still is today.

This tremendous gap in advancement between proptech and fintech is clearly reflected in the venture capital funding: in the year 2015 when real estate tech was just starting, proptech companies received only $2.21 billion of funding while investments in financial technology totaled $46.7 billion.

And although investments in proptech companies hit $32 billion last year, real estate remains one of the most technologically underserved industries, largely because of highly fragmented infrastructure, frequent compliance checks, and vast stakeholder ecosystem.

At the same time, it is one of the most transaction-heavy asset classes. In 2021 alone, $3.6 trillion was exchanged in the US from the acquisition and sale of real estate.

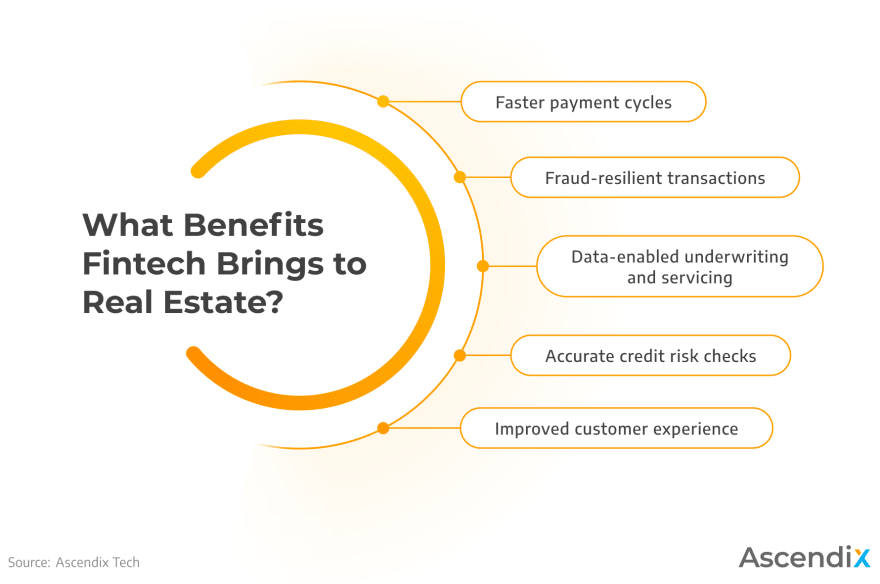

The undertechnologized nature of real estate coupled with tremendous transaction volume creates vast opportunities for real estate fintech companies to address significant, unsolved pain points devouring transactional efficiency in real estate for decades. Specifically, the application of fintech in real estate means:

- Faster payment cycles. By leveraging proptech trends such as blockchain and tokenization, fintech real estate companies can dramatically speed up the transaction periods, so that something like mortgage deposit processing that used to take 3 working days can now be nailed down in a matter of seconds.

- Fraud-resilient transactions. Real estate fintech companies like Zepto provide account-to-account payment platforms that don’t need to connect to a sponsoring bank nor use a 3-rd middleman to process a payment, thus eliminating any data breaches and fraud activity.

- Data-enabled underwriting and servicing. As the integrated fintech in real estate expands, inducing new technologies like Big Data and Artificial Intelligence, real estate owners and investors will leverage data better to improve their underwriting and servicing models.

- Accurate credit risk checks. With enhanced client data aggregation, landlords are always equipped with information about the client’s financials to be sure whether they can afford the rent, just as lending banks can estimate if the borrower can afford the loan.

- Improved customer experience. With the generational shift in homebuying toward millennials (source), the modern, digitally native homebuyers, armed with mobile devices, now expect a seamless, digital experience for their banking needs. This is something that real estate fintech companies need to catch up on with their elder counterparts fintechs.

How to Develop a Disruptive Proptech Fintech Solution?

Although there are clear signs of positive disruptions in real estate transactions, many pain points remain unsolved. Buyers and sellers still struggle to navigate the fragmented landscape of physical space, relying on offline and insecure payment systems, while banks, appraisers, investors, and brokers are torn between merciless workstreams.

As I have already pointed out earlier, these inefficiencies actually play into the hands of fintech real estate innovators wanting to inject new lean operational structures and new value propositions into how real estate transactions are managed. Without real estate expertise not technical background, however, this would be barely possible.

Having operated in the real estate business for 16 years as a software developer and technology consultant, Ascendix took time to get smart about the pain points in the traditional transaction management and the ways to tackle them with cutting-edge proptech and fintech solutions. If you don’t have internal resources or real estate knowledge but have a revolutionary proptech fintech idea in mind, it is worth considering partnering with us because:

- As real estate product developers ourselves, we have an extensive solution portfolio and do know all the nuances of bringing innovative ideas to life from scratch

- Headquartered in Dallas, the US but having 3 more offices worldwide, we combine our local, national and international experience to deliver disruptive real estate fintech software at reasonable rates and around the clock

- We are honored to have partnered with real estate titans like JLL and Colliers

- We have distinctive experience building innovative Cloud Applications that deliver exceptional agility, performance, and interoperability to real estate fintech firms.

Top comments (0)