Personalizing the checkout experience is important especially if you want to build a website with a checkout experience that won’t become one of the 70% of shopping carts that are abandoned. Whether you're building a native application or web app, giving your customers a better experience during checkout will improve your overall conversion rate and success. Offering the right payment methods to your customers without interruption, and designing for synchronous and asynchronous payment types on your platform can give you a leg up in the global economy.

What is a Synchronous and Asynchronous Payment Flow?

Synchronous payment flow means that the payment is completed at the same time as the HTTP request and response. This typically happens with some credit or debit card payments. For example when a card payment is made in the US, the response and webhook notification will immediately give a final success or error response.

Asynchronous payment flow refers to all the scenarios when the payment is not completed in real-time, but rather at a later point in time. The immediate response to the payment request is not the final confirmation, and extra steps are needed before the final payment completion. For example: using 3DS cards where additional cardholder verification is required, subscriptions payments, third party payment methods, fraud/risk checks, and more.

Any asynchronous event should be handled using a webhook event where it would notify clients, and provide info to notify the end user. Webhooks are notifications that are set up to contain all relevant information about the event that triggers it. Webhooks can also be used to confirm any payment response given in a synchronous event.

Types of Asynchronous Payments

There are several different types of asynchronous payments, including:

Two-Step or Delayed Payments

Payments that are delayed until a specific event occurs, such as the delivery of goods, escrow, or service start dates.

3DS Payments

Card payments in certain countries require 3DS (3D Secure) verification, which adds another layer of authentication for the customer to verify their card for the purchase.

Payment Redirects

Payments that include bank transfers, or local ewallets that require the user to be redirected to their account login to make the payment. These can also include future payment services like crypto or any third party payment provider.

Recurring Payments

Payments that occur on a regular basis, such as monthly subscription fees or automatic bill payments.

Installments

Payments that are broken up into multiple smaller payments, such as a payment plan for a large purchase.

Group or Split Payments

Payments that are paid by, and/or paid to more than one person, for example, a ride sharing app with two people paying one ride. The payment is also split up and sent to the driver and the ridesharing company in different accounts.

Benefits of Asynchronous Payments

Implementing asynchronous payments can provide several benefits for both the business and the customer. Some of the key benefits include:

Improved Customer Personalization

Asynchronous payments can help you retain customers by making it easy for them to pay in their payment method of choice. Whether it is a subscriptions model, ewallet, credit card or bank transfer they want to pay with, the customer has options.

Increased Convenience

Asynchronous payments allow customers to set up automatic payments, but also delay or split their payment at a certain time when the product is delivered.

Improved Cash Flow

Asynchronous payments can help businesses better predict and manage their cash flow. A steady stream of recurring payments help with subscriptions, offering the right payment options, but also splitting payments into two different wallets to conveniently payout employees.

Challenges of Asynchronous Payments

While asynchronous payments are absolutely essential and beneficial, there are also some challenges to consider when implementing them. Some of the key challenges include:

Complexity of Network

Asynchronous payment systems can be complex, with multiple stakeholders and processes involved. This can make it difficult to manage and maintain the system.

Security

Asynchronous payments involve storing and processing sensitive financial information, which can increase the risk of data breaches and fraud. PCI (Payment Card Industry Data Security Standard) Compliance is necessary when handling sensitive customer payment information.

Integration

Asynchronous payments may need to be integrated with various platforms, such as billing and invoicing platforms, which can be time-consuming and require specialized expertise. Integrating with all different payment systems for a global audience can slow down expansion to new countries and customers.

Best Practices for Building and Managing an Asynchronous Payment Platform

To ensure a successful implementation of asynchronous payments, there are several best practices that developers should follow:

Use a Secure Payment Gateway

Choose a payment gateway that is secure and compliant with industry standards, such as PCI DSS.

Test the Platform Thoroughly

Thoroughly test the payments for your platform to ensure that it is reliable and able to handle the volume of transactions. Make sure you can test in a sandbox mode and make the same payments successfully in production. Having a strong support service to rely on is helpful, and also a greater community of developers.

Monitor and Manage the Network Uptime

Regularly monitor and manage the payment network’s uptime to ensure that it is functioning properly and that any issues are promptly addressed. Having a team that continually monitors uptime, daily operations, and a strong support service is critical at the right time.

Keep the System Up-to-date

Stay up-to-date with industry developments and best practices, and make sure to keep the payment system updated with the latest security measures.

One API for Synchronous and Asynchronous Payments

Building a payment system from scratch is hard. Expanding your payment network at the speed of how fast you’d want your global business to grow can be nearly impossible. Using a payment provider with an all-in-one payment API can be easier than building and maintaining your own service.

Rapyd, is an API first company on a mission to liberate global commerce with all the tools you need for payments, payouts and business everywhere. Rapyd manages an API with both synchronous and asynchronous payment methods.

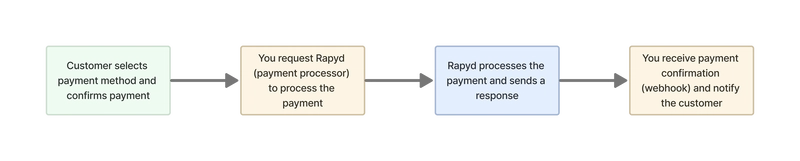

For example a general high level payment flow may look like the following:

What happens between the immediate payment response in blue and the last webhook payment confirmation may depend on the payment type, or synchronous / asynchronous payment flow.

You can use an API only solution to build a more customized payment flow, redirect / embed to a hosted checkout page to cover all your PCI compliance requirements, or simply include a link to a secure checkout page on your website, or email campaign to your subscribers.

Conclusion

Asynchronous payments are a convenient and efficient way for businesses to process payments and manage their cash flow. However, implementing and managing an asynchronous payment system can be complex and requires careful planning and attention to detail. By following best practices and choosing secure and reliable payment gateways, developers can build and manage successful asynchronous payment systems that provide value to both the business and the customer.

Delivering an experience that meets the needs of each unique market is crucial to building a thriving international ecommerce business. Reducing cart abandonment begins with designing around the customer. Creating checkout experiences with a global audience in mind is the first step toward a best-in-class site, app and checkout process anywhere you do business.

Using a third party payment provider with one API can help you focus on your checkout experience while having the burden building a payment network lifted.

Top comments (0)