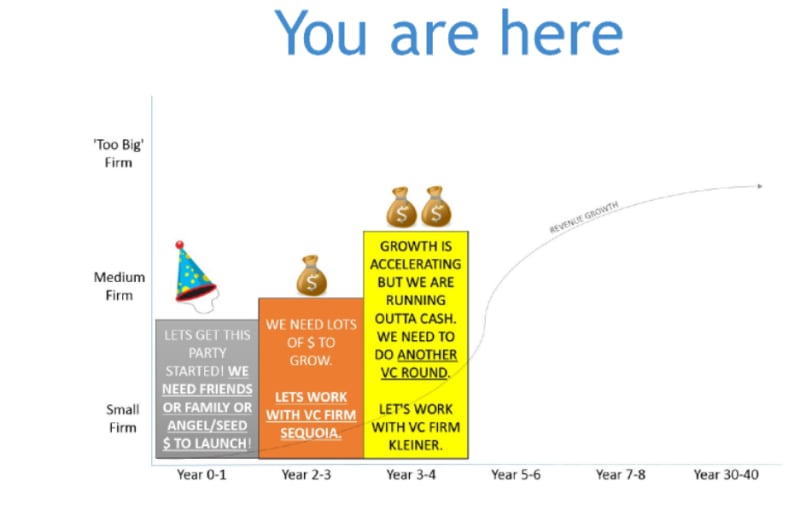

So we're now in years 3 to 4 on our journey, in terms of what's next after this. After this eventually we'll get ready to go public.

Let's learn from a situation:

Assume this famous athlete created Paypal and submitted it's Proof of Concept to venture Capitalists

So he's got kind of a test version, or a proof of concept version of this terminal.

Okay?

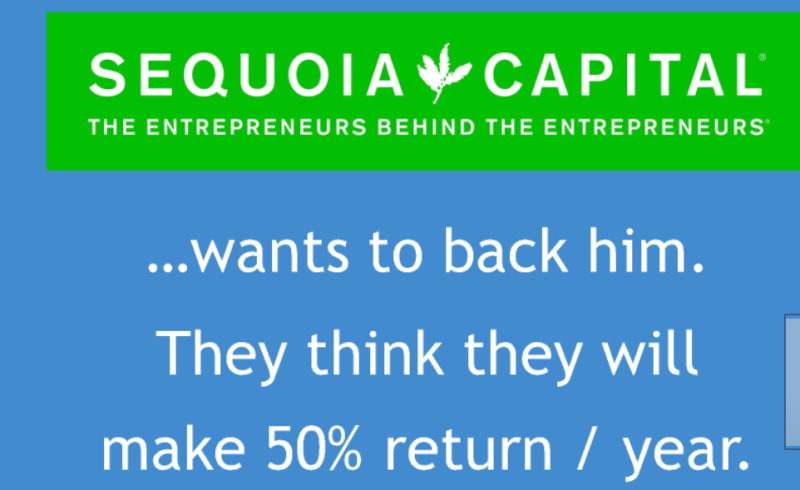

But he needs a million bucks to build a real version of it, not just a prototype version, a real version. And so, here comes Sequoia. And Sequoia is the best hedge capital firm in the world and they wanna back him.

Initially, Giancarlo launched his payment company, last year he had $10,000 in equity capital, or of his own money, okay?

And he decided to launch the company then last year with 2 million shares, okay? Don't over think this, just accept, 2 million shares, right?

Now,

He needs to negotiate with Sequoia on how many shares they are going to get in his company in return for money that he can use to fund his growth.

So Sequoia and Giancarlo agree that in 5 years his company is gonna make a million bucks in net income, that's pretty good, five years from now, he'll make a million bucks.

Okay, a competitor of Giancarlo's just went public, just an initial public offering, okay? And this competitor did this at a valuation of 20 million dollars, and this competitor had 2 million dollars in income. That means the price range ratio is 20 million valuation, the price, divided by the earnings, 2 million, 10 times.

A 10 times p/e multiple,

So in five years,

Giancarlo wants to go public as well, okay? And so the valuation of his company in five years should be as follows. If the competitor of Giancarlo's firm is public, and trades at 10 times earnings, then his firm should trade at 10 times earnings in five years.

Giancarlo's firm is gonna make a million bucks. And that means a valuation of 10 million (10*1 million [earned in 5 years]) bucks in five years.

In five years, his company will be worth 10 million dollars.

So what is his firm worth today?

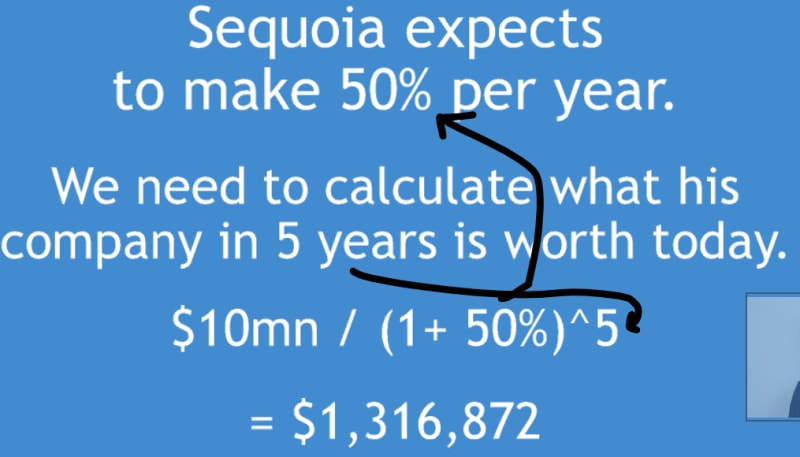

So here's how we get there. Sequoia expects to make 50% per year, okay? So we have to calculate what his company

in five years is worth today. So again in five years, his company is worth 10 million bucks, and Sequoia is only gonna invest if they can make 50% return every year, okay?

So, here's the math. So we discount that 10 million bucks to today. And the way you discount, and we'll cover this during our DCF

we're discounting that 10 million bucks. The value of his company in five years, to today. And we're doing it at Sequoia's expected rate of return, which is 50%, okay?

So, currently

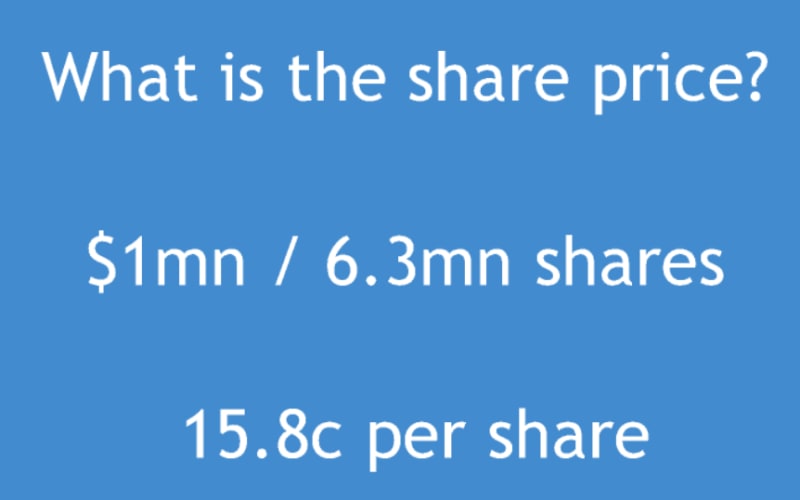

So the value today is that Sequoia owns a million bucks worth, remember they're investing a million bucks?

Divided by 1.32 million (Valuation this year), so they own 76% of the company.

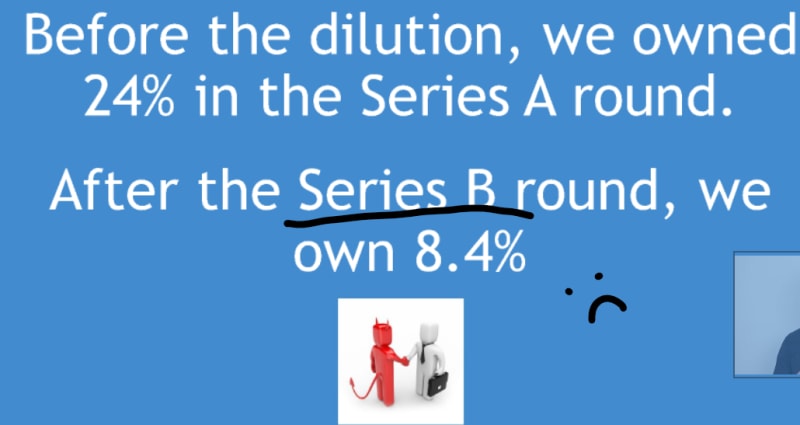

So that means the owner own 24%, okay? Or Giancarlo owns 24%.

And he's got 2 million shares initially, right?

Now, let's learn how much he has left with

So total shares is 2 million divided his .24 (24%), which equals 8.3 million shares, it's just math.

2000000%(.24)=8333333.33 shares = 8.3 million shares

That means Sequoia owns 6.3 million shares.

8.3 million (now shares) - 2 million ( initial shares) = 6.3 million shares

So the share price is 15.8 cents per share. That's what the share price is. Right?

1000000 (Sequoia invested 1 million) % *6.3*1000000) million shares ( Sequoia ownes 6.3 million shares now) = $ 0.158730 = 15.8 cents

So how much does Giancarlo own?

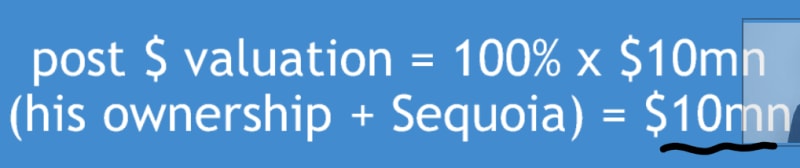

Well he owns 2 million shares (Initially started with this) times 15.8 cents per share. Right, which is $316,000 dollars. This is called the pre money valuation of his company, right?

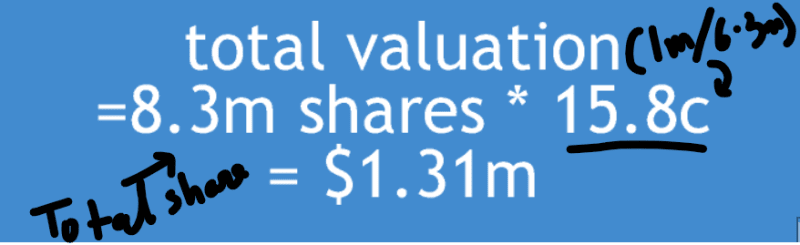

And then the total valuation of the company is 8.3 million shares (Previously total shares is 2 million divided his .24 (24% owned by the owner now), which equals 8.3 million shares,).

You know, his 2 million plus Sequoia's 6.3,

time 15.8 cents, which equals 1.31 million dollars!!

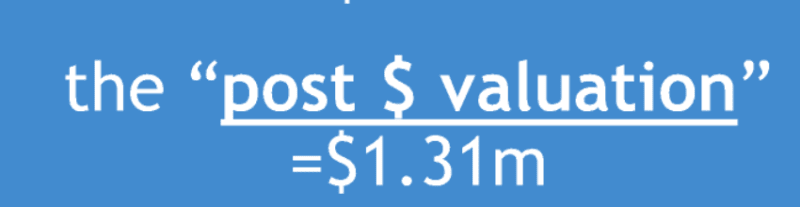

So the post money valuation, the value of the company after the money was given from Sequoia is 1.31 million dollars.

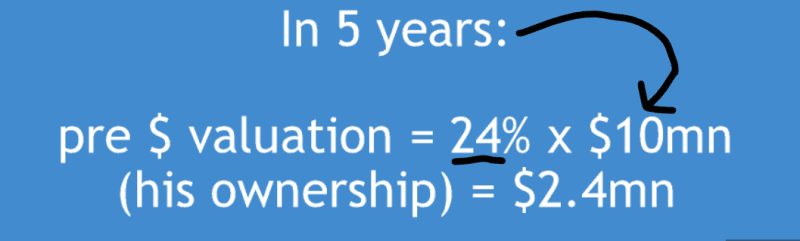

So, in 5 years, the company worth is going to be 10 million dollars and he has 24% of the company and he will be worth $2.4 millions now

Unless anything goes wrong!

After the valuation, it is 10 million dollars

So Sequoia just led what's called the A round, or the first round, okay?

Giancarlo (The owner) just did an A round with Sequoia, lucky him, Sequoia's awesome.

Uh oh, oh shoot.Breaking news!!!

So, what happened was

Giancarlo (The owner) got injured, right? This is a bit of a setback, he's gonna be okay, he got injured.

Okay, so something happened,

Giancarlo got hurt, his company got hurt.

Okay?

So now we're in year three and we need more money. Shoot, we ran out of money faster than we thought we would.

Alright, so. Cash is king, okay?

So, we did the A round with Sequoia in year one, okay? And in year five we wanna go public, right? And then Kleiner is now, the second venture capital firm, and they're leading the B round, okay?v

So, we're in year three, and we need another million bucks, yeesh.

We still wanna go public in year five at a valuation of 10 million dollar

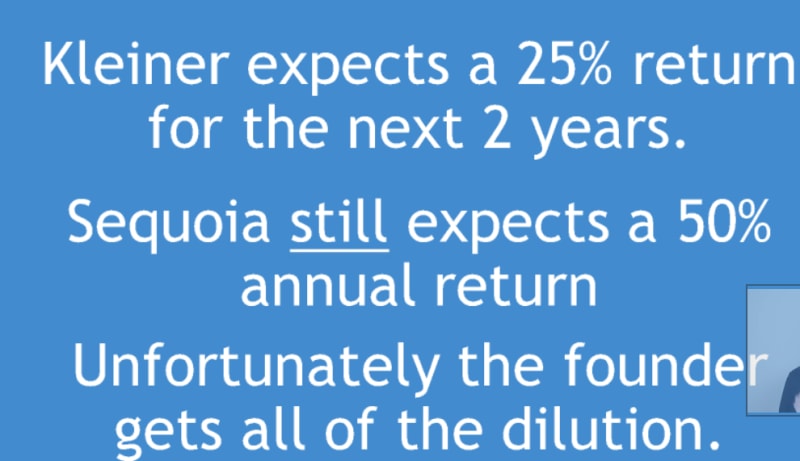

So Kleiner expects a 25% return for 2 years until the company goes public. How did they come up with the map?

Well Sequoia still expects a 50% annual return, and unfortunately,

Kleiner Perkins, which is a great firm and so is Sequoia, and what they're doing in this hypothetical example it's not their fault, it's the banner's fault. But Kleiner Perkins needs shares, right?

So Kleiner's expected return is a million bucks, and thus they are

investing a million bucks now at 25% return over 2 years.

Which means that in 2 years, their million dollar investment is 1.5625 million dollars, okay?

1000000 ( 1 million Kleiner is investing) * (1+25%)^2 = 1.5625 Million

Here they are expecting 25% return and in 2 years because within 2 years, this company is going to be public.

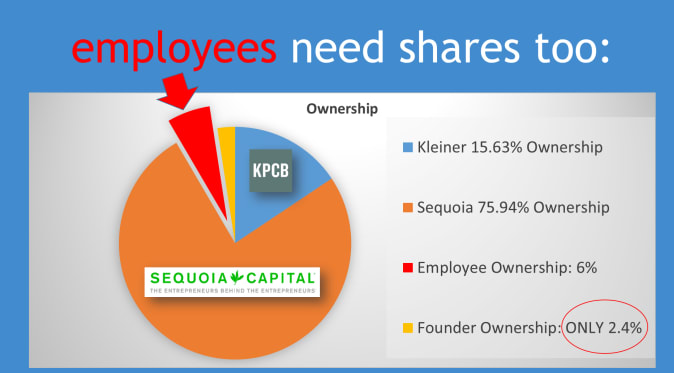

So Kleiner's ownership is 1.56 million dollars divided by 10 million bucks or 15.6%, okay?

Sequoia remains there shares and lost nothing

But the owner becomes the victim and comes in dillution.

So our ownership, or Giancarlo's ownership goes from 24%, to 8%.

So, how many shares are available now???

So, sequoia now have 18 million shares

As, 24 million shares new exist and 76% is owned by sequoia

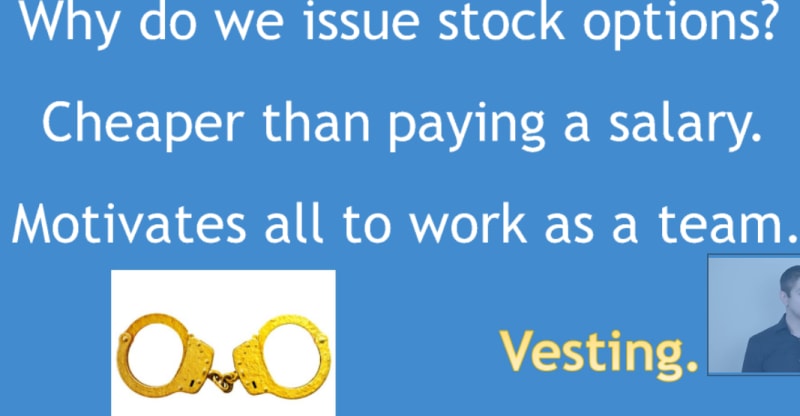

It actually gets worse because, we as Giancarlo forgot about employee ownership via stock options, remember,

you always want to incentivize employees, right? By giving them options, right?

And these options only vest or become valid or you're allowed to cash them in every four years.

So it's the golden handcuffs keeping you in place as an employee.

Alright let's move on. So, employees need shares too.

So, right now, we had to give 6% of shares away to employees, and remember we owned 8.4% of the company? Well now that we have to give 6% of shares away to employees because we forgot to include that in our legal documents early on, we only own 2.4% of the company now, that's tragic, tragic!!

It's not Sequoia's fault.

It's not Kleiner's fault.

It's my fault, I'm Giancarlo.

why do we issue stock options?

Well, it's cheaper than paying a salary, because we don't have that much money, right? So I'm gonna give my employees part of the company. It motivates everybody to work hard as a team, and it's basically golden handcuffs. And there's something called vesting, which means, you can't benefit from ownership in stock options until you've held them for four years, okay?

They vest. Vest every four years.

So, the company have 82 million shares now!!

And the options (That we give to employees; their percentage is 6%) are that many shares,5 million shares, so,

we got diluted by 90%, yeesh!

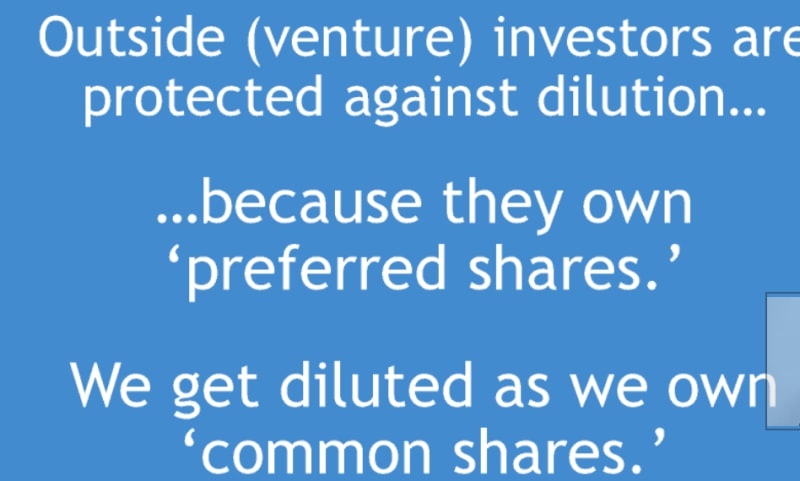

outside venture capital investors are protected against dilution.

Why?

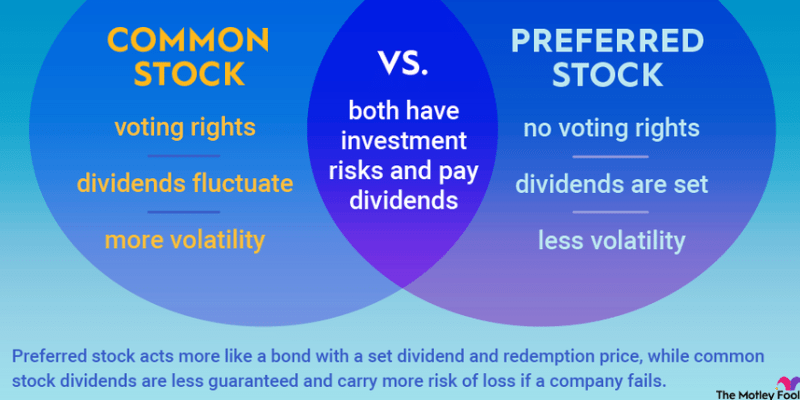

Because they own preferred shares, they're preferred. We get common, (Giancarlo gets common) Okay?

Don't know what is common share and what is preferred?

Read this out

And so, you need lawyers, you need lawyers. And founders of companies really need to understand dilution before dealing with venture capital firms.

It's not all that bad though, because founders of companies get massive option grants anyway, and, every year, like Larry Ellison would get a lot of options every year,

So, he could actually, hypothetically speaking, be worth a heck of a lot more, if the value of his company goes up materially after the IPO. It works out well.

But you do get diluted, just keep in mind, if you deal with a venture capital firm, or equity investors as opposed to banks, you're gonna give up ownership of your company.

But hopefully your company's worth a lot more money over time so it becomes a moot point.

But don't, don't do debt, if you're an early stage company, because if you have one little hiccup like we just did here with Giancarlo, you're done, you're done, banks don't care.

If you miss one payment, they'll screw you, they'll take everything.

But it's okay, because you're protected, and so is your family, because you have an LLC, or a limited liability corporation structure set up.

A lot of the most successful entrepreneurs in the world have failed many, many times, before they succeeded.

Michael Jordan once had this great quote. He's the best basketball player of history, of course, in history, he said that,

"I failed many, many times in life,

"and that is why I succeeded."

So venture is very hard, in order to return the capital on a 400 million dollar fund, you have to have 20% of your funds or two unicorns in your fund, it's really, really tough,

the Silicon valley is where all the old school companies are, right by Stanford. Ebay, Google, old school, I know. Yahoo!, Oracle, EA.

And all the cool new companies are up in San Francisco there, like Airbnb, or Uber, or Salesforce. AppDirect, Udemy of course, which is an awesome company by the way

Read this called Internet Trends

So, we are done!

Top comments (0)