Introduction

The Blockchain technology gained a lot of popularity lately, partly thanks to cryptocurrencies like Bitcoin. In a previous article, I explored several possible use cases for the blockchain technology outside of the cryptocurrency realm. In this article, I will explain what a blockchain would look like to become more relevant and sustainable for businesses. A blockchain designed for a business network will still be a distributed ledger based on a peer-to-peer network, but there are some key differences between a blockchain supporting something like Bitcoin and another built for a business network.

Assets over cryptocurrency

Because the Bitcoin's blockchain was built specifically for cryptocurrencies, it took some time to realize that we could use blockchains for something else than cryptocurrencies. Instead of using a token in the shared ledger ( bitcoin, ether... ), any other asset could be used. Are cryptocurrencies really useful for businesses to run their operations? Building trust, improving security, reducing costs and delays, these are the things a business will look for when using a blockchain. Private blockchains don't need a token or coin to operate.

Identity over anonymity

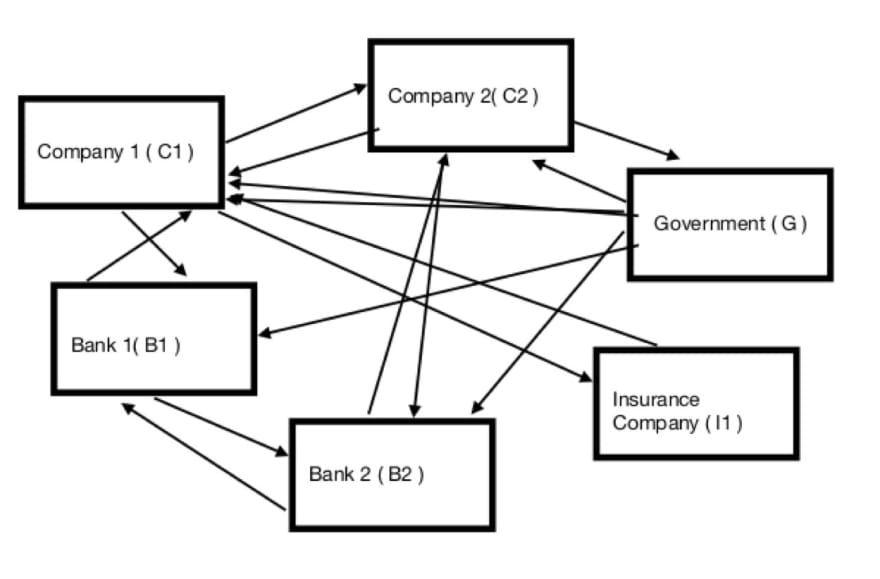

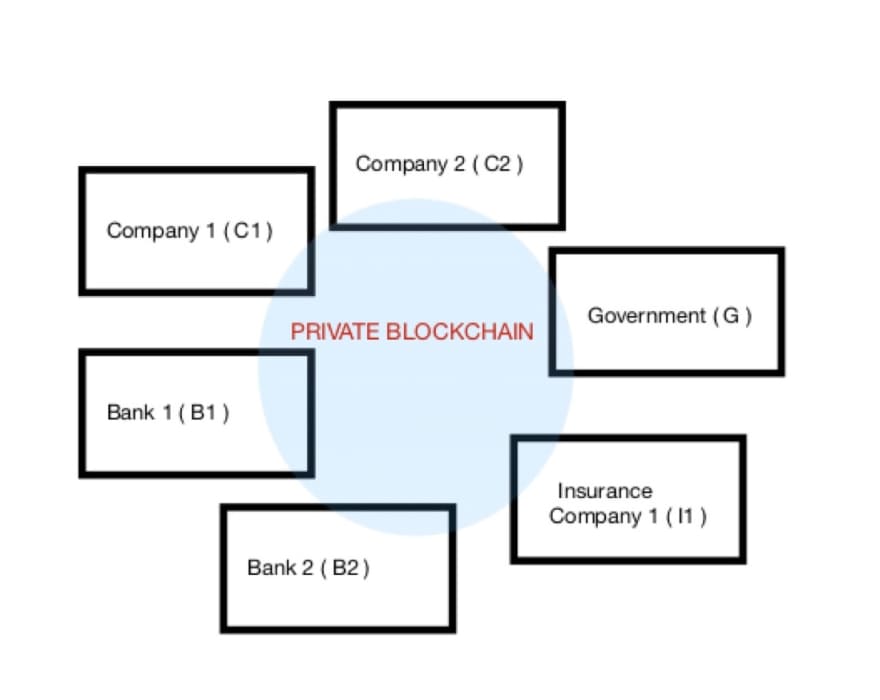

In Bitcoin, everybody is anonymous. You don't know who you are sending your bitcoins to, or receiving bitcoins from. In a private blockchain, anonymity is not what you need. You need to know where the money is coming from, and you need to know who your customers are. You need privacy, not anonymity. Let's use a example of a simple business network:

In a normal network, each entity would have its own ledger, its own record of transactions. Which means that everytime a transaction occurs in the network, each entity concerned by the transactions would have to update their ledgers. If company C1 buys from company C2 and company C1 needs a loan from bank B1 and an insurance from the insurance company I1, every single one of those organisations would need to update their books. This is not an efficient way to do things.

With a blockchain, only one ledger would be updated. But, contrary to the Bitcoin blockchain, not everybody can see everything. By implementing an authentification system, company C1 can only see the transactions that it is involved in. The company would have access to the complete details of the transaction it made with C2, the loan with B1 and the insurance with I1. C1 would not have access to informations about C2 transactions ( if C1 is not involved ), or the banks in the network ( assuming C1 is still not involved ).

Privacy, not anonymity.

Selective endorsement over proof-of-work

In Bitcoin, and other blockchains, we verify transactions through mining. The whole network has to work to confirm transactions and blocks are safe. In a private blockchain in a business network, we would use selective endorsement. The network would choose who controls, verifies and confirms transactions within the network. Going back to the previous example, the transaction between C1 and C2 could be controlled by C1's bank and C2's bank. You could choose any number of entities to verify transactions in the network.

Four Requirements

In simpler terms, a blockchain designed for a business network needs to meet four requirements:

Shared Ledger: Every actor in the network shares the same ledger. It is append-only. Can't modify or delete a past transaction.

Smart contracts: Every business has rules. In a blockchain, you would write smart contracts. Basically, you take a business rule and translate it into code that gets executed with each transaction. For example, if company C1 ships a product to a customer, I could write code to make sure that C1 and the shipper are paid only when the customer received the product. We could also write rules that would define the conditions of a loan. The examples are infinite.

Privacy: As I said earlier, privacy over anonymity. We still need to know who we are dealing with. Transactions are still secure, verifiable but authenticated. You are still going to have a fair share of cryptography.

Trust: A key component, we achieve trust by choosing which participant endorse transactions. Because transactions can't be modified or deleted later, we have a reliable audit trail.

Benefits

How a business would benefit from a blockchain?

- Time: Transactions would be a lot faster. We could go from days to real time.

- Costs: Less intermediates and overheads.

- Risks: Prevents tampering, fraud and cyber-crime.

- Trust: Increases trust thanks to shared record keeping and processes

Conclusion

Blockchains go way beyond the cryptocurrency world. I'll even make a prediction by saying it will transform the global economy in the future. Blockchain is a very young technology still, and we have only scratch the surface of what will be possible, but the future looks bright.

Top comments (4)

I have the hope as Blockchain developer that 2018 is the year of Blockchain without cryptocurrencies, the year in which we start focusing on applications instead on token value. We'll see.

Amen to that!!

Hey Damien!

Have you heard of keeex.me/ ? They were founded in 2014, they provide electronic signature and more

Haven't heard of them, but will check it out :)